Ignacia Mercadal

Financial speculators have a controversial role in commodity markets. Though they are expected to bring benefits like higher liquidity and informational efficiency, they are often accused of increasing prices and manipulating markets. This paper studies the role of financial traders in electricity markets, where they effectively compete with physical producers and restrict their market power. Using data on MISO, the wholesale electricity market of the American Midwest, I show that financial players can lead to lower prices and increase consumer welfare.

In wholesale electricity markets, financial players trade alongside physical buyers and sellers of energy, which is possible because these markets are organized as sequential markets. There is first a forward market that schedules production a day in advance, and then a spot market to adjust unexpected shocks right before operation. Financial traders buy (sell) in the forward market and then their transaction is reversed in the spot market, as if they would sell (buy) the same amount. Therefore, their profits depend on the difference between the forward and the spot prices.

A forward premium, i.e. a higher price in the forward market, has been documented in several markets around the world. This forward premium comes from generators’ market power, i.e. their ability to affect prices by changing the quantities they offer (Ito and Reguant, 2016). When producers have market power, they have incentives to sell less than their intended production in the forward market, in order to increase the price, and then sell the remaining production in the spot market at a lower price, a strategy that results in a higher forward price.

Generators typically have market power because electricity cannot be stored, demand is not price responsive and has to be met by supply at every moment, and limited transmission capacity does not always allow to cover demand with the cheapest generation. These characteristic features of electricity make it scarce, and though financial players do not increase the amount of energy produced, they are able to restrict producers’ market power by arbitraging the forward premium.

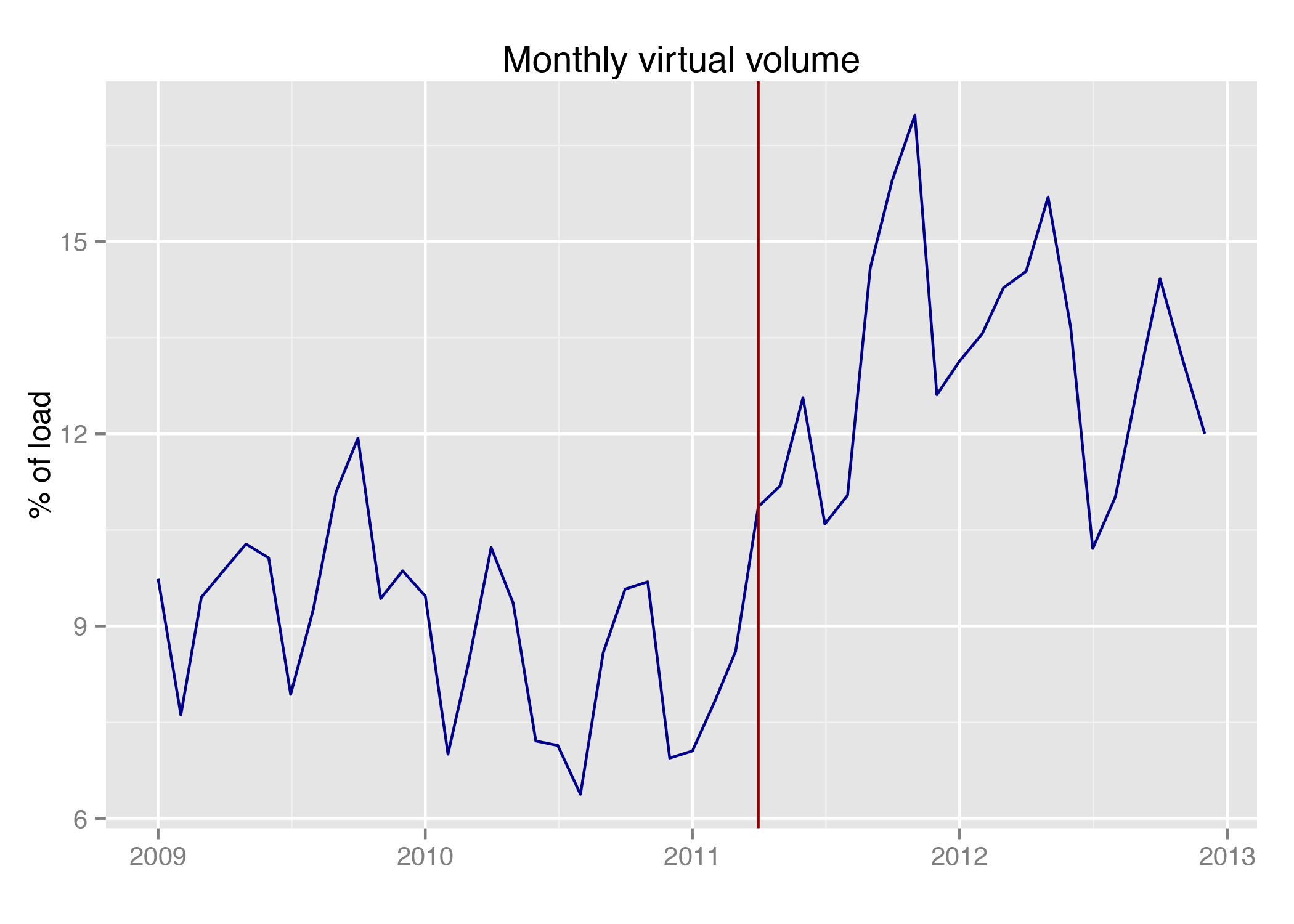

Because a forward premium leads to inefficient planning and higher production costs (Jha and Wolak, 2018), many makets have introduced financial traders in order to arbitrage this forward premium. In the MISO electricity market the premium persisted in spite of the presence of financial traders because high transaction costs prevented them from fully arbitraging it (Birge et al., 2018). On April 2011, these charges were significantly lowered, and financial trading increased significantly, as Figure 1 (below) shows.

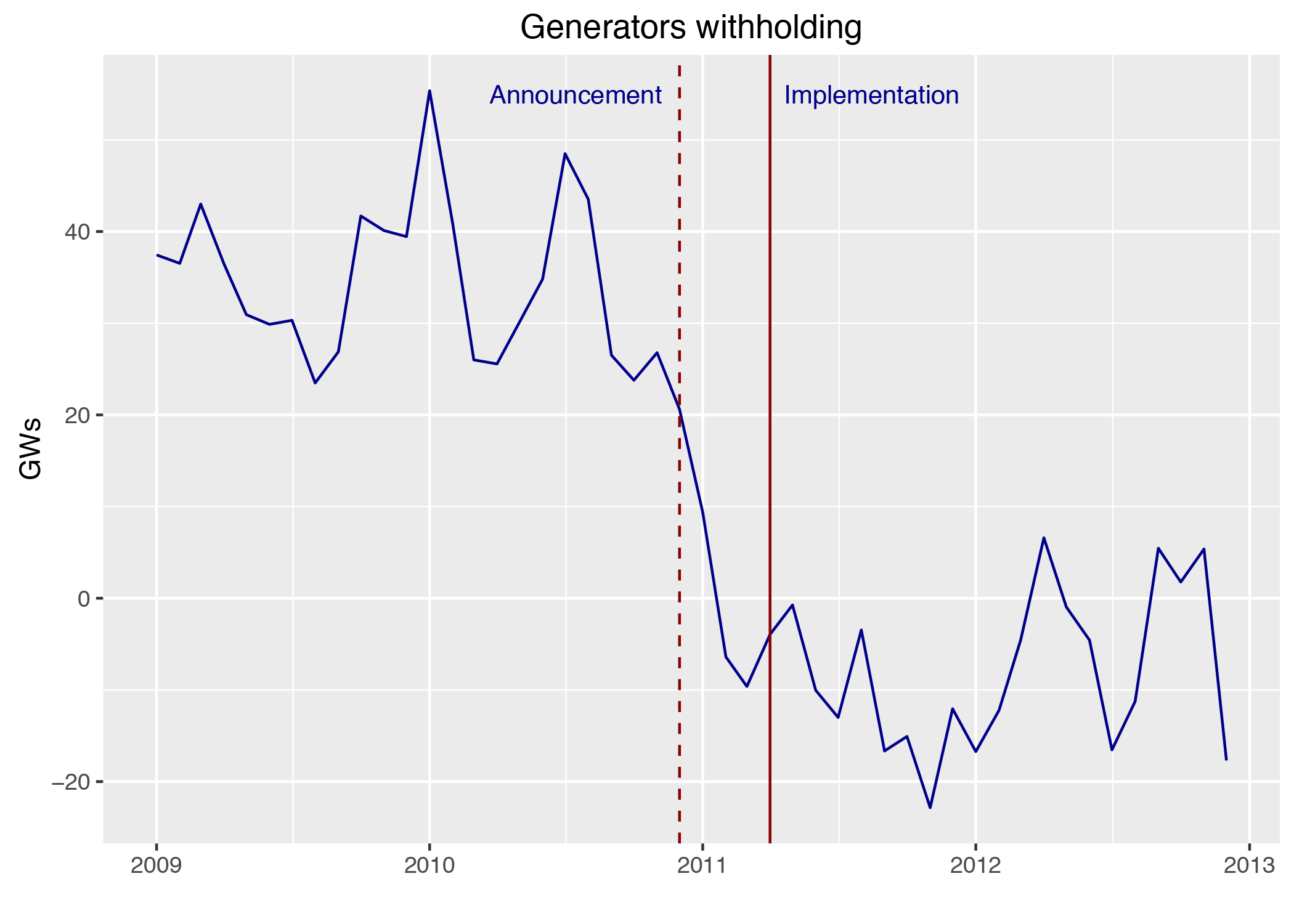

While transaction charges were high, generators exerted market power by withholding sales in the forward market (Figure 2, below). Moreover, they did not only exert less market power in the forward market in response to increased financial activity, but they did so when the regulatory change was announced, months before it was implemented. This behavior is surprising since firms only lose market power when financial trading became cheaper, not at the time of the announcement.

In order to understand the generators’ anticipated response, I estimate a static model of optimal behavior for a generator deciding how much to sell in the forward and spot markets. This requires to estimate the demand faced by each firm, for which it is necessary to who are the firm’s competitors, i.e. it requires to define the market in which each firm participates. This is not straightforward in a nodal market, where prices vary across over 2000 nodes or locations according to the capacity of the transmission grid that transports electricity. As I do not observe locations, I use machine learning tools to define markets according to price correlation and develop a measure of fit that indicates they accurately represent the competitive structure of the market.

Results indicate that the firms’ anticipated response to increased financial arbitrage is consistent with tacit collusion. Firms are able to cooperate only as long as they know that the agreement can be sustained in the future, but incentives vanish when they learn this will not be possible in the future. Consumers are better off because they pay less for the same quantity, saving roughly $1,800,000 a day on average.

References

Birge, J., A. Hortaçsu, I. Mercadal and M. Pavlin (2018) “Limits to arbitrage in electricity markets: A case study of MISO.” Energy Economics

Hortaçsu, A., and S. Puller (2008) “Understanding Strategic Bidding in Mult-Unit Auctions: A Case Study of the Texas Electricity Spot Market,” RAND Journal of Economics

Mercadal, I., (2018) “Dynamic Competition and Arbitrage in Electricity Markets: The Role of Financial Players”, MIT CEEPR Working Paper 2018-015.

Ito, K., and M. Reguant (2016) “Sequential markets, market power, and arbitrage.” American Economic Review.

Jha, A. and F. Wolak (2018) “Testing for Price Convergence with Transaction Costs: An Application to Financial Trading In California’s Wholesale Electricity Market”

Further Reading: CEEPR WP 2018-015

About The Authors