CEEPR Working Paper

2026-04

Santos J. Díaz-Pastor, Carlos de Abajo, Robert Stoner, and Ignacio J. Pérez-Arriaga

Universal electricity access remains a development priority and a climate enabler. Yet the global trajectory still falls short. IEA projections suggest that about 645 million people could remain without electricity by 2030, with more than 80 percent in Africa (IEA et al, 2025). Africa also needs a sharp increase in capital inflows, on the order of $23 billion per year between 2025 and 2035, to meet access targets (IEA, 2025). The main barrier is no longer the lack of least-cost planning tools. It is the difficulty of turning technically coherent plans into financeable investment programs.

Modern geospatial electrification algorithms have achieved unprecedented analytical precision. Today, these computational tools can seamlessly delineate the economically optimal deployment of grid extensions, localized mini-grids, and stand-alone systems down to the household level, offering highly granular spatial resolutions that were previously unattainable. Governments and development partners now use these tools to define national roadmaps. Many of these roadmaps then stall at implementation because planners treat finance as an exogenous input, not as an outcome of regulation, utility performance, and payment security. Recent work has shown how ignoring financing assumptions can bias electrification outcomes and understate implementation constraints (Agutu et al., 2022).

This working paper proposes an integrated regulatory and financial framework that addresses this issue. It links three components that often sit in separate conversations. It starts from a least-cost plan that produces a detailed time profile of capital and operating expenditures across on-grid and off-grid options. It then assigns clear implementation responsibilities through licenses or concessions, with a universal service obligation, and places these responsibilities under cost-of-service regulation. It finally designs a financing architecture that coordinates public resources, concessional instruments, and commercial capital in a way that matches cash needs over time.

The context matters for bankability. In many low- and middle-income power sectors, distribution companies face chronic financial distress. Governments cap tariffs for affordability. Utilities also lose revenue through technical losses, weak billing, and low collection. These frictions create quasi-fiscal deficits and deter investment (Foster and Rana, 2020). They also raise perceived risk and the cost of capital. On African power projects, risk premiums and interest rates can be two to three times those in advanced economies. Private finance then concentrates on generation projects with contracted revenues, while networks and last-mile delivery lag.

Cost-of-service regulation provides a disciplined way to define what it should cost to deliver service and what an efficient operator should earn. The regulator calculates an allowed annual revenue requirement. It includes efficient operating costs, depreciation of invested assets, and an allowed return on the regulated asset base. This revenue requirement is not a planning aspiration. It is the benchmark that investors and lenders use to assess revenue adequacy and credit risk.

Implementation depends on a simple cash logic that many plans leave implicit. Each year, an operator must receive enough cash to cover the allowed revenue requirement. Customer tariffs can provide part of that cash flow, but affordability constraints often bind. When customer payments fall short, a supplementary payment must be made to cover the difference in a timely and predictable way. Annual revenue reconciliation is imperative to bridge the gap between allowed revenues and what the operator can actually collect.

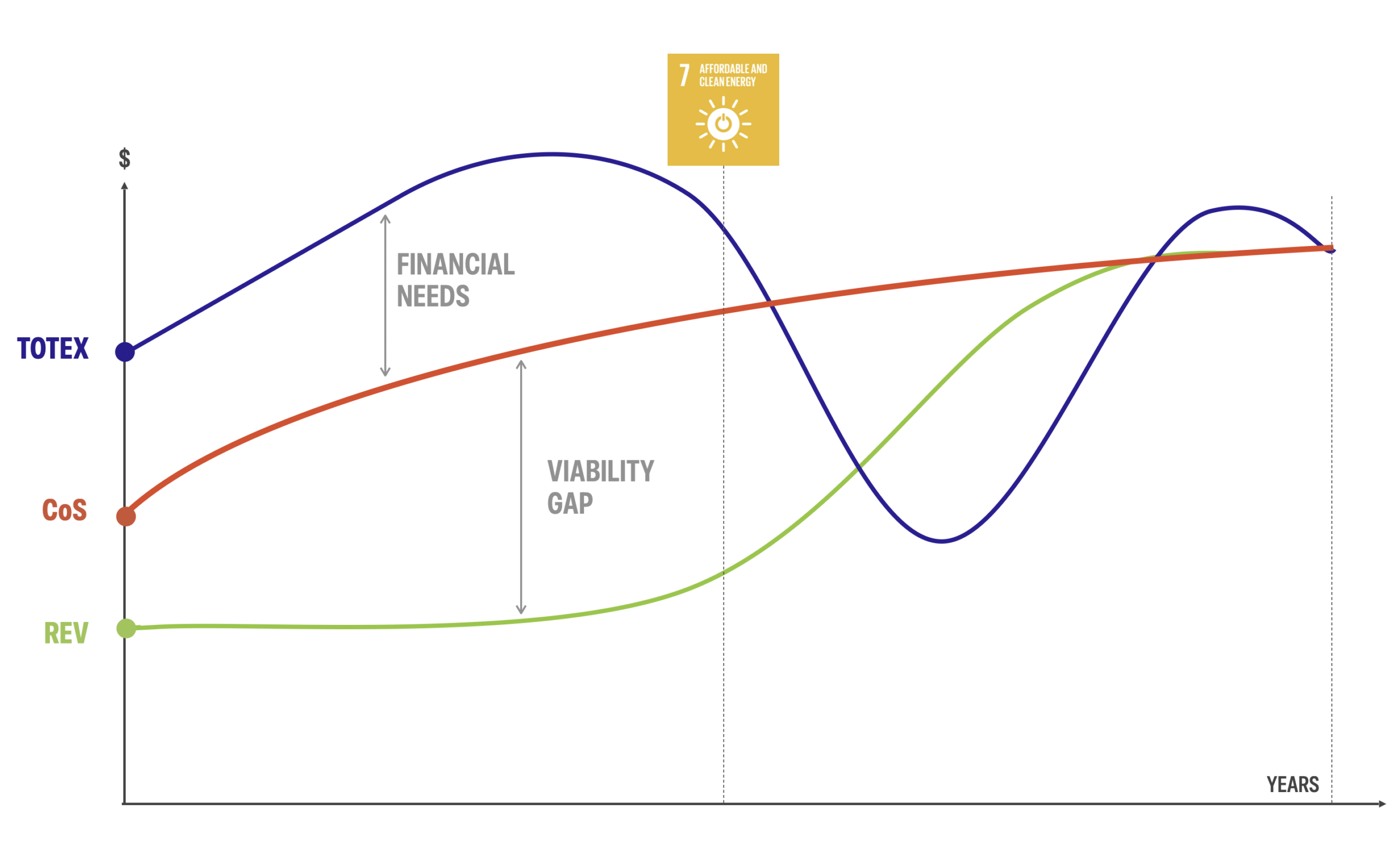

This cash-flow view separates two distinct constraints that can be seen in Figure 1. The first is the viability gap. It arises when affordable tariffs and weak retail performance imply that cash revenues remain below the regulated cost of service over the relevant horizon. In that case, the business is structurally unable to recover efficient costs. No financial engineering can fix that problem. Policymakers must either raise revenues, reduce efficient costs, or provide explicit compensation that is rule-based and predictable.

The second constraint is financing needs. It comes from timing, not from long-run profitability. Electrification requires front-loaded capital expenditures and working-capital outlays. Cost-of-service regulation recognizes these costs over the useful life of the assets, through a regulated revenue requirement that spreads recovery over time. In practice, the regulator does not “pay back” CAPEX in the year it is incurred. Instead, it allows (i) depreciation, which returns principal gradually, and (ii) a return on the undepreciated regulated asset base (RAB), which compensates the investor for tying up capital. Revenues therefore follow the path of regulated cost recognition and tariff pass-through, while the operator pays real cash costs upfront when it builds lines, installs transformers, or deploys off-grid assets. This intertemporal mismatch between cash outlays and regulated revenue accrual creates early-year cash deficits and liquidity stress even when the program is viable in present value terms. The key point is that “profitability” is assessed over the asset life, but lenders and suppliers require cash in the construction and ramp-up years.

Figure 1. Evolution of revenues (REV), regulated costs (CoS), and total expenditure (TOTEX) over time.

These two constraints require different instruments. Viability gaps require an explicit and credible compensation mechanism. This mechanism can combine targeted budget transfers from the general government budget, earmarked resources through an access fund that can be capitalized by the state, donors, or levies, or regulated cross-subsidies within the tariff system. The instrument matters less than its credibility as a predictable cash-flow commitment. If payments arrive late, remain discretionary, or are exposed to annual appropriation uncertainty, investors will price that risk, and the cost of capital will increase. Financing needs instead require bridge finance and capital structures aligned with the regulatory recovery schedule. Longer tenors, grace periods, sculpted debt service, and liquidity facilities can keep early-year cash deficits from becoming implementation failures.

The framework treats delivery models as technology-neutral. Grid extension, mini-grids, and stand-alone systems all face the same economics when governments expect them to provide permanent service. Each implementing agent needs a stable revenue model anchored in efficient costs and enforceable service standards. For off-grid provision, this implies a “utility-like” approach rather than a pilot logic. Competitive procurement and concessions can still play a central role. They can allocate territories and reveal the minimum subsidy required to meet a defined service standard, while regulation anchors long-run revenue adequacy.

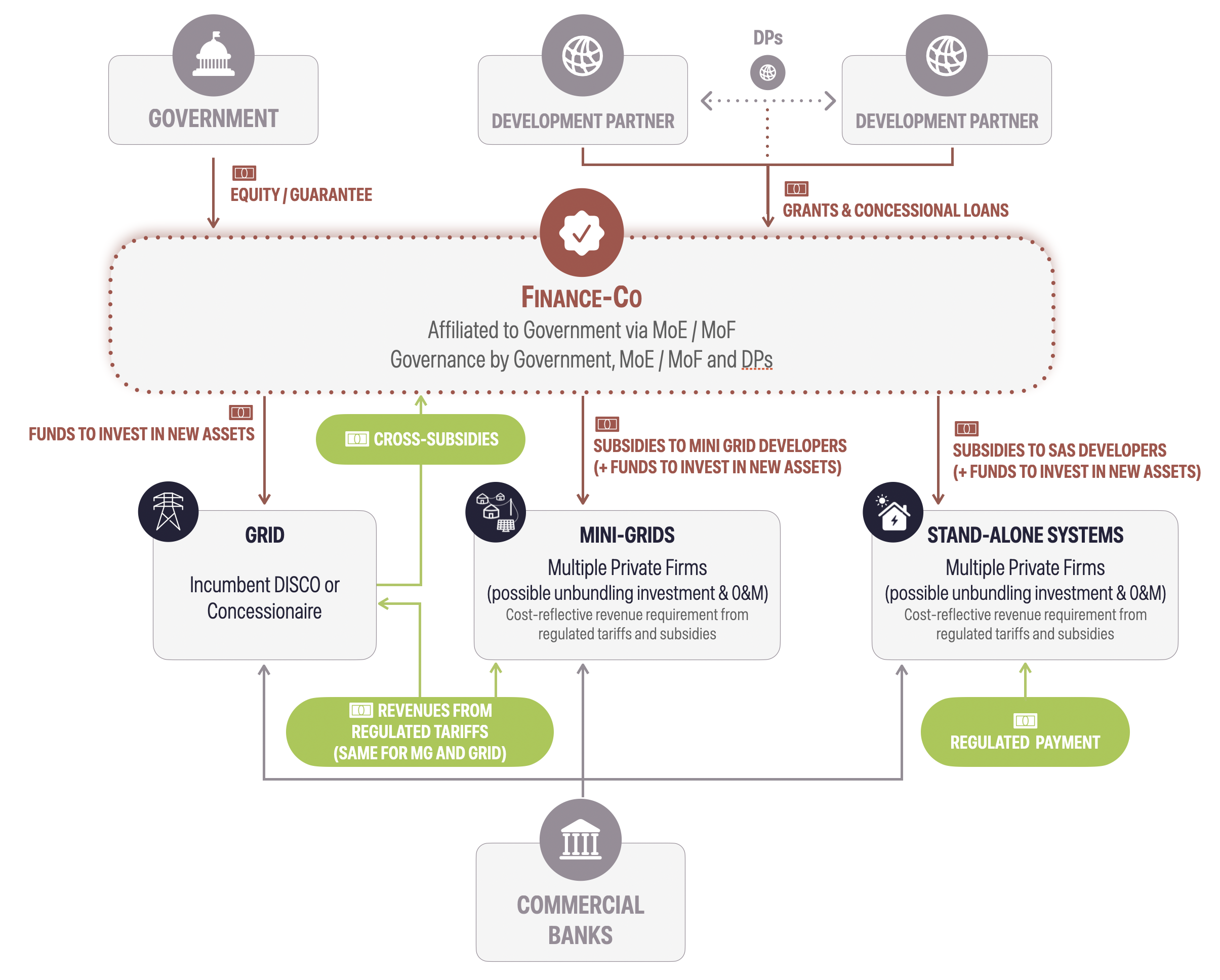

A central contribution of the paper is a financing architecture that can operationalize these principles at scale. As defined in Figure 2, we propose a pooled platform (“Finance-Co”) that consolidates public resources, development finance, and sector-based cross-subsidies. Finance-Co ringfences inflows and standardizes disbursement rules. It channels funds to grid, and off-grid implementers based on verified delivery and the annual revenue reconciliation described above. This design reduces fragmentation across donor programs, improves transparency, and strengthens payment security.

Figure 2. Stylized cash flow structure of an integrated financing vehicle for universal electrification, showing funding sources, subsidy channels, and implementing entities across grid extension, mini-grids, and stand-alone systems.

Finance-Co does not replace strong regulation. It strengthens it by making cash transfers auditable and predictable. It also creates a natural home for blended finance. Concessional loans, guarantees, and grants can reduce the sector’s effective cost of capital and lower the long-run burden on tariffs and budgets. The platform can allocate these instruments to the specific constraint that binds. Grants and recurrent transfers address the viability gap when affordability is structurally binding. Liquidity facilities and long-tenor debt address financing needs during rollout.

The policy message is direct. Least-cost planning remains necessary, because it reduces the investment requirement and the subsidy envelope. It is not sufficient. A plan becomes implementable only when it specifies enforceable obligations, a transparent annual revenue reconciliation, and a financing structure that covers early-year cash deficits. This paper provides a replicable methodology to do that in a way that is consistent with affordability and fiscal constraints. The full working paper formalizes the cash-flow metrics and the institutional design choices. It is intended as a practical guide for regulators, ministries of finance, development partners, and investors who need universal access plans that can actually be financed and delivered.

Link to the full working paper:

MIT CEEPR Working Paper 2026-04

About The Authors