CEEPR Working Paper

2026-02

Kimberly A. Clausing, Christopher R. Knittel, and Catherine Wolfram

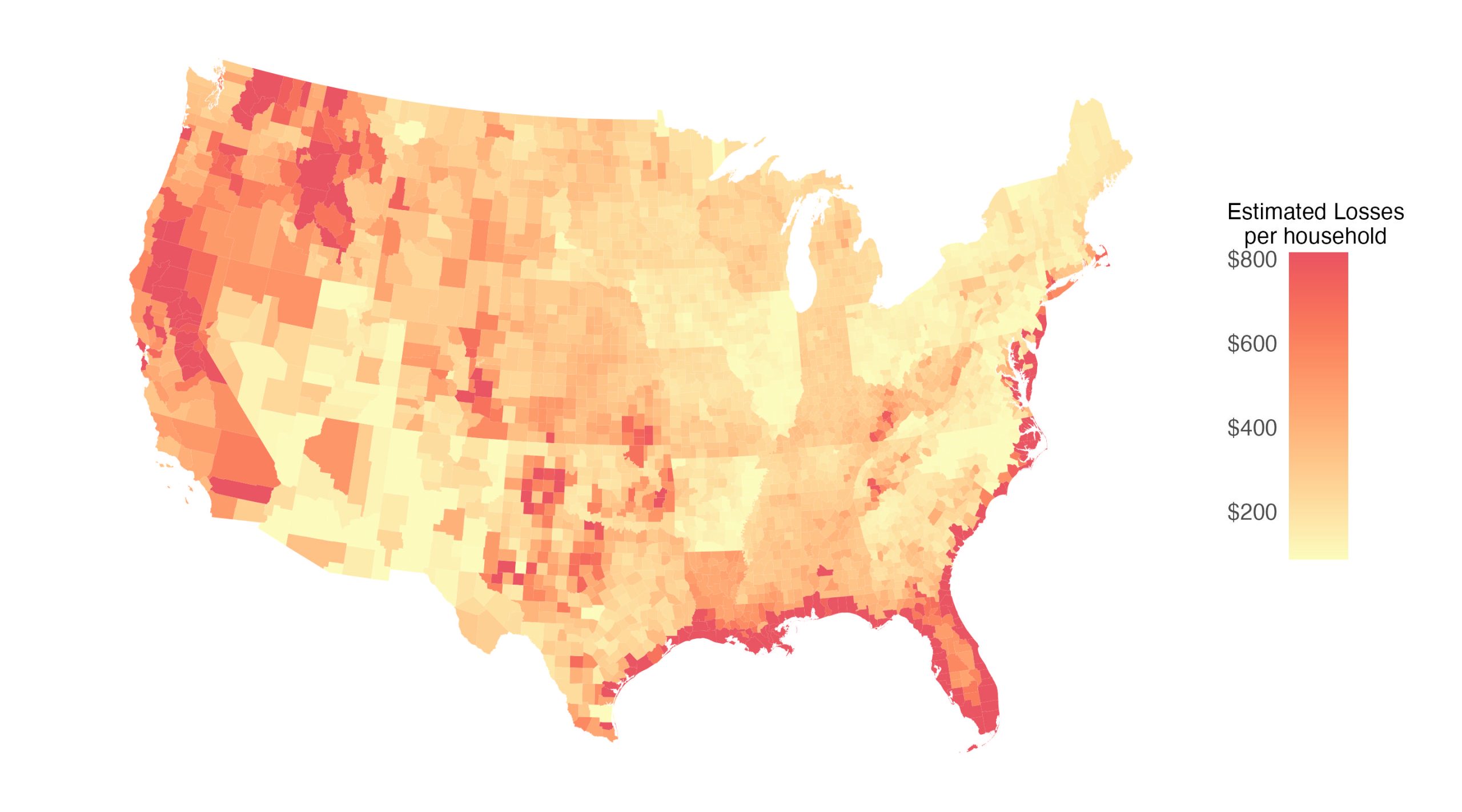

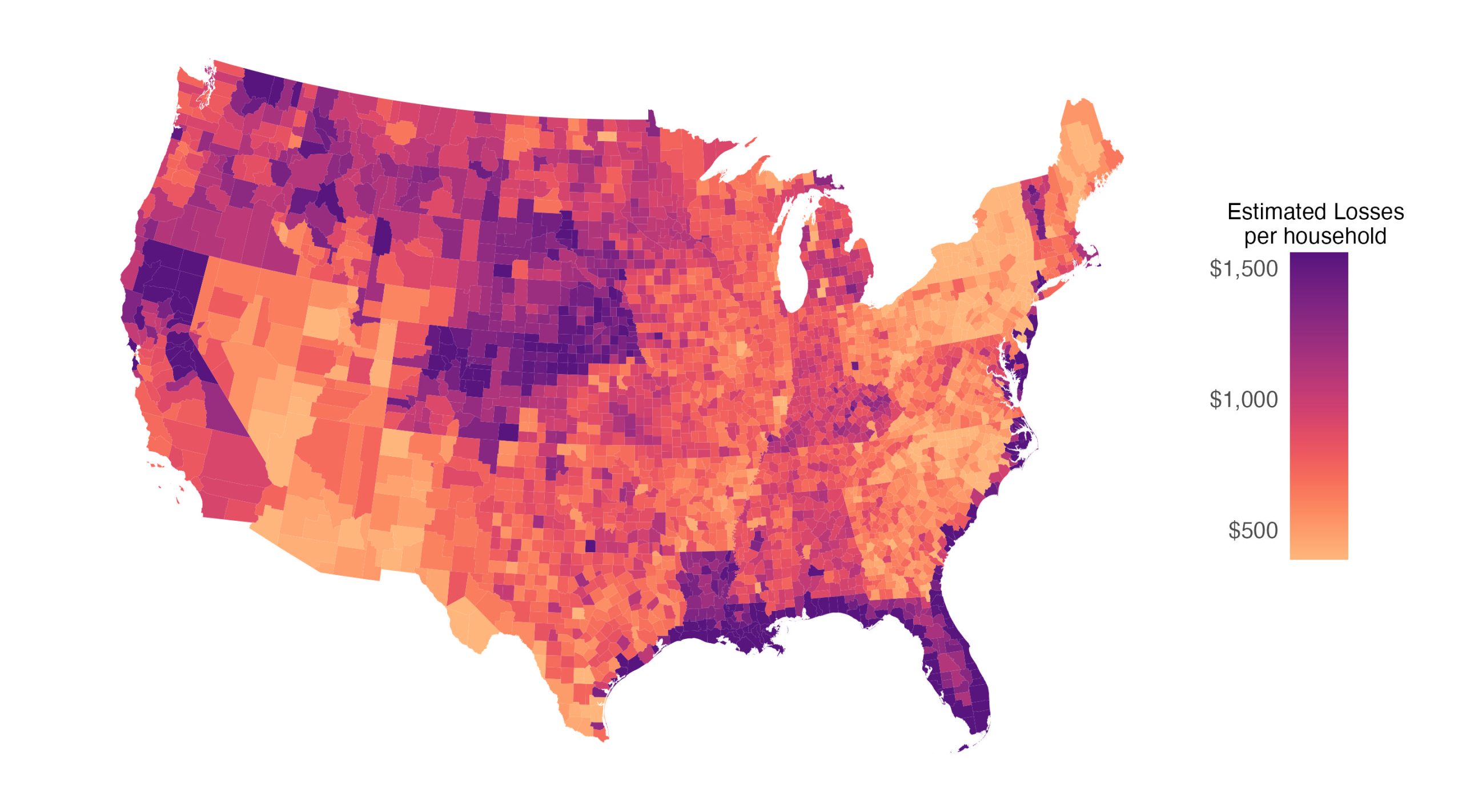

Climate change is no longer a distant threat—it is already imposing substantial and uneven costs on U.S. households. A new study seeks to quantify these costs across multiple channels, including household budgets, mortality, and public spending. While the authors examine only a subset of climate-related impacts, the evidence suggests that recent climate change now imposes an average cost between $400 and $900 per household annually depending on attribution assumptions, with the hardest-hit counties exceeding $1,300 per household. These burdens are highly uneven, falling disproportionately on low-income households and regions exposed to extreme weather and wildfire smoke.

Extreme Weather as the Dominant Cost Driver

A central finding of the paper is that extreme weather events—not incremental warming—account for most household burdens today. Over the past three decades, the United States has experienced rising frequencies of billion-dollar disasters, from hurricanes and floods to wildfires and severe storms. These events create financial pressures through higher insurance premiums, infrastructure disruptions, and utility price increases, while also imposing significant threats to life.

Although heat exposure has increased across most U.S. counties, its net effect on mortality remains small. In many regions, declines in cold-related mortality have roughly offset increases in heat-related mortality. By contrast, wildfire smoke and extreme weather events have created sharp increases in mortality and financial damages, and these trends have accelerated over the past decade.

Insurance Markets: A Growing Financial Strain

Household insurance premiums have risen rapidly, particularly in disaster-prone regions. Drawing on mortgage escrow data from Keys and Mulder (2024), the authors estimate that climate-driven increases in hazard risk have raised homeowners’ insurance costs by an average of $73 per year under more conservative assumptions and up to $356 per year under less conservative attributions to climate change. These increases are notably higher in the South, Gulf Coast, and wildfire-prone West.

These estimates exclude major perils—such as flooding and storm surge—that are not covered by standard homeowners’ policies. Supplementing with First Street Foundation data, the authors find additional flood- and wind-related losses that households implicitly bear through either insurance gaps or taxpayer-funded programs. When indirect commercial pass-through is included, insurance-related costs rise by another $32–$145 per household.

The distributional pattern is stark: losses are relatively flat in dollar terms across income groups but sharply regressive when viewed at its share of households’ income.

Energy Expenditures: Modest Physical Use Impacts, Large Price Effects

Climate change affects household energy spending in two ways:

1.) Changes in the quantity of energy used (driven by shifts in heating and cooling needs).

2.) Changes in the price of energy (driven by disaster-related infrastructure costs).

Using machine-learning models applied to RECS microdata, the authors estimate that warming since 1990 has increased cooling expenditures by $25–$33 per household, while reducing winter heating bills from natural gas, propane, and kerosene, resulting in a net but modest increase in energy consumption of about $11 per household. The more significant effect comes from utility rate increases.

Disaster recovery, wildfire mitigation, and storm hardening have placed new financial burdens on electric utilities, which are increasingly passed on to ratepayers. Based on electricity price models using NOAA disaster data, households now pay an additional $30 per year on average for electricity due to climate-related infrastructure costs—with some regions, such as the South and West, experiencing increases above $150–$200 per year.

These energy cost increases are also regressive: low-income households devote a larger share of their income to energy and have fewer adaptation options.

Public Expenditures and Taxpayer Costs

Governments also bear significant costs from climate-related disasters which the authors measure through the disaster relief outlays dedicated towards infrastructure repair, social insurance programs, and ad hoc emergency assistance to affected households and firms. By aggregating FEMA, HUD, state, and local expenditures from 2017-2021 and delineating allocations for storm- and wildfire-related disasters, the authors find that the between $41 and $77 of the taxes paid by the average American household go towards these relief efforts. Since these disbursements are ultimately funded by taxpayers, the greater frequency of catastrophic events may induce greater tax burdens which themselves vary greatly across states.

Mortality Impacts: Wildfire Smoke Dominates

The mortality effects of climate change differ sharply across geography. While heat-related mortality has changed only modestly (though higher among Black Americans and low-income individuals), wildfire smoke has emerged as a major and rapidly growing health threat.

Using updated particulate-matter exposure data from Childs et al. (2022) and quasi-experimental mortality estimates by Deryugina et al. (2019), the authors find that wildfire smoke contributed to over 35,000 deaths in 2024, with an average annual household mortality cost of $100 attributed to climate change. These mortality outcomes are concentrated in Western states and disproportionately harm lower-income counties highlighting regressivity in particulate matter impacts.

These estimates include only mortality. Because emergency department visits, hospitalizations, medication use, and lost workdays are excluded, the true health cost is significantly higher.

Conclusion: Climate Change Is Already Costly— and Unequally So

Across insurance markets, energy bills, public infrastructure, and health outcomes, the authors find that the costs of recent climate change are substantial, growing, and regressive. The most consequential impacts today come not from incremental warming but from extreme weather events and wildfire smoke, which disproportionately affect vulnerable households and regions.

Even under conservative assumptions, the analysis suggests that climate inaction already costs U.S. households tens of billions of dollars each year. As extreme weather intensifies in coming decades, these burdens are likely to increase dramatically unless mitigation, adaptation, and resilience measures keep pace.

(a) More Conservative Estimate (winsorized at 95%)

(a) Less Conservative Estimate (winsorized at 95%)

Figure 1. Aggregate costs per household by county.

Link to the full working paper:

MIT CEEPR Working Paper 2026-02

About The Authors